Take our short survey to see how much money you qualify for.

CELEBRATING 19 YEARS OF EXCELLENCE

We are proud to be America’s #1-rated HUD-approved lender celebrating 19 years of excellence.

THE LEADER IN LOWER RATES PER HUD DATA

The Department of Housing & Urban Development (HUD) publishes average interest rate data for the public for each Home Equity Conversion Mortgage (HECM) lender.

LOWER RATES MEAN MORE $ FOR YOU

Since interest rates are a primary factor in determining how much money you can receive, borrowers with the lowest rates typically receive more proceeds and overall benefits from their reverse mortgage. In addition, lower rates mean better performance of equity retention over the life of the loan. We encourage you to compare!

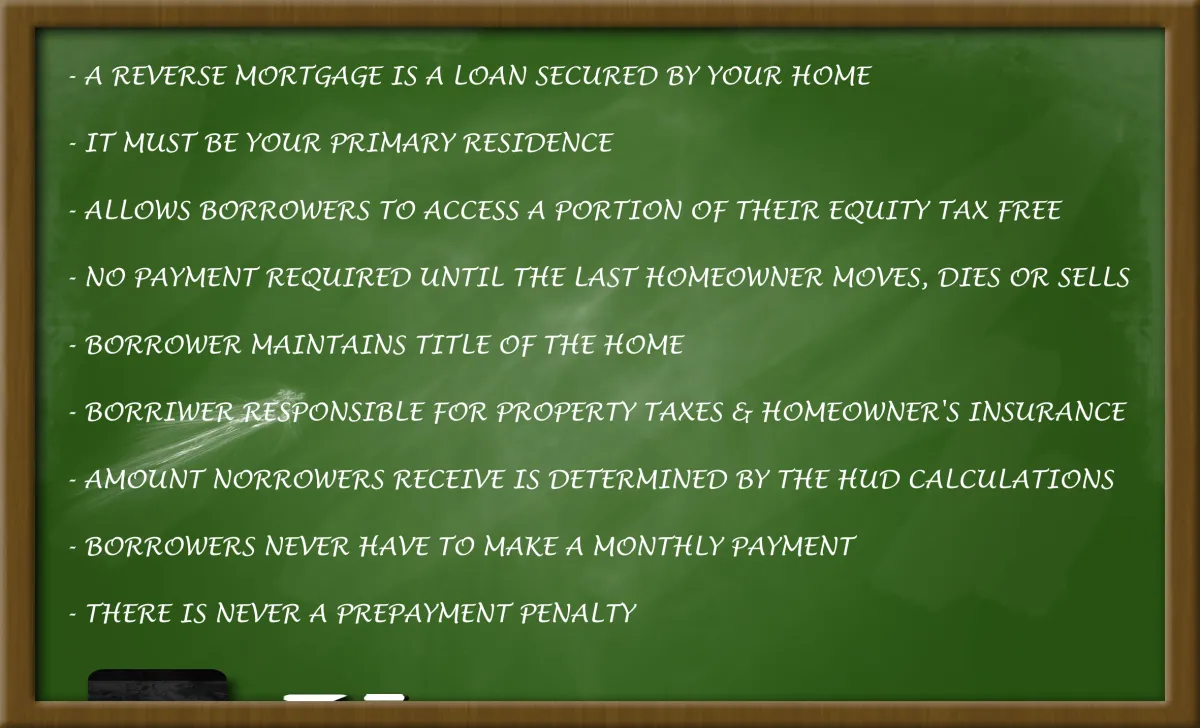

WHAT IS A REVERSE MORTGAGE?

A reverse mortgage is a loan secured by your home. The home must be your primary residence (that means that you, the borrower, must live in the home for as long as you have the loan). This type of loan allows borrowers to access a portion of their tax-free equity without making monthly mortgage payments.

No payment is required until the last surviving homeowner moves, dies, or sells the home.

The borrower maintains the home’s title and is responsible for property taxes and homeowner’s insurance payments. The amount borrowers receive is determined by the HUD calculations based on the age of the borrowers (specifically, the age of the youngest borrowing or non-borrowing spouse ), the value of the home, or the HUD lending limit, whichever is less, and the interest rates in effect at the time.

Borrowers never have to make a monthly payment on reverse mortgage loans.

There is never a prepayment penalty, so they can make any payment they wish, including repaying the loan at any time.

IS A REVERSE MORTGAGE RIGHT FOR YOU?

Reverse mortgage loans are not suitable for everyone. There’s also a downside to reverse mortgages. It may surprise you to hear a lender say this, but it is true.

If you are looking for a short-term loan, you may be better suited for a different type of financing.

A reverse mortgage loan can sometimes require closing costs and upfront mortgage insurance premiums, making it impractical as a short-term solution in some cases.

However, for those who wish to remain in their homes and need extra cash flow, the HECM may be precisely what you are looking for. We explain

how a reverse mortgage works and answer many frequently asked questions and common misconceptions.

Educate yourself or your family on the safeguards with our pros and cons guide.

.

HOW IS A REVERSE MORTGAGE REPAID?

Reverse mortgages require no monthly payments as long as the borrower(s) lives in the home. The loan becomes due and payable when the last borrower on the original loan permanently leaves the property because they died, they have permanently moved to an assisted living facility or with family for care, or the borrower sold the home.

The loan becomes due and payable at that time and must be repaid. There are several things borrowers and heirs of reverse-mortgage borrowers should do in anticipation of needing to finalize or pay off the loan.

We recommend that you take the following steps:

Procure the title in the names of the heirs. This can include adding the names of heirs even before the borrowers pass away. Your reverse mortgage allows you to add persons to the title if at least one original borrower remains on the title. Probate may be required after borrowers pass away, so we recommend that you seek professional counsel from an estate attorney in advance to determine the best method for your circumstances and state laws.

Contact a local real estate professional to determine the most probable selling price of the home.

Compare the value or most probable selling price with the loan’s outstanding balance.

Decide if you want to refinance the loan, pay it off with other funds, or sell the property once you have all your information. If there is equity in the home based on the value and most probable selling price, you would pay off the balance of the loan, but remember, heirs also have the option to pay 95% of the home’s current value if the balance exceeds the value and if you still want to keep the home.

A reverse mortgage is a non-recourse loan. Suppose your heirs do not want to keep the property or sell it. In that case, they can let the lender take the property back, and the lender’s only recourse is the property itself.

The lender cannot look to other assets to repay the obligation. Your heirs will owe nothing, even if the loan balance exceeds the property value.